With this last piece of domestic data before the Bank of Canada’s policy announcement next week, the GDP report is positive news on a few fronts.

Marwa Abdou

With this last piece of domestic data before the Bank of Canada’s policy announcement next week, the GDP report is positive news on a few fronts. With a surprise contraction of 0.2% in real GDP in the second quarter, the economy has clearly slowed in response to monetary tightening. Given the recent inflation report, where July saw inflation exceed 3% after a period of steady cooling — drifting further from the BoC’s 2% target — this is the positive news many had hoped for and increases the likelihood of the Bank holding rates steady.

Marwa Abdou, Senior Research Director, Canadian Chamber of Commerce.

KEY TAKEAWAYS

Headline

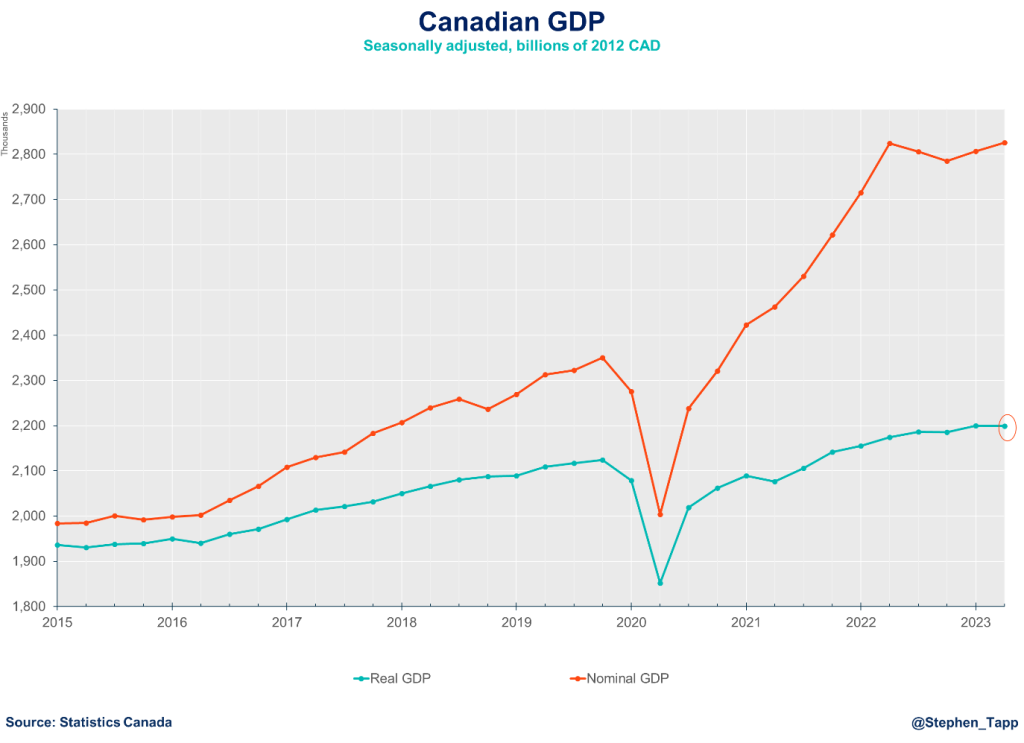

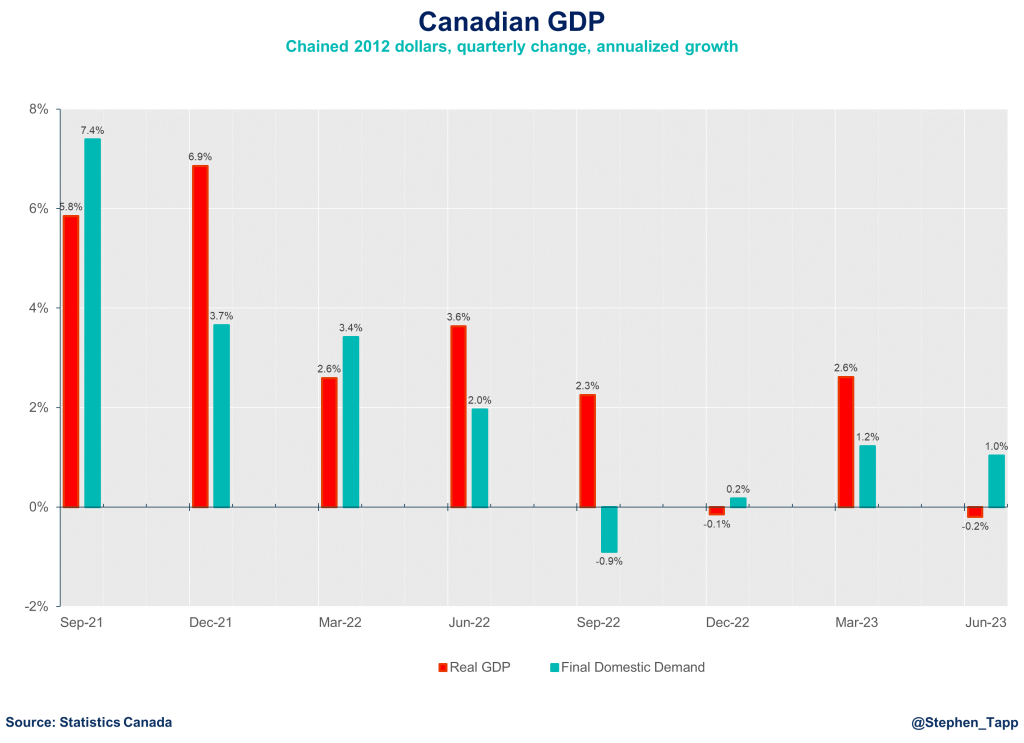

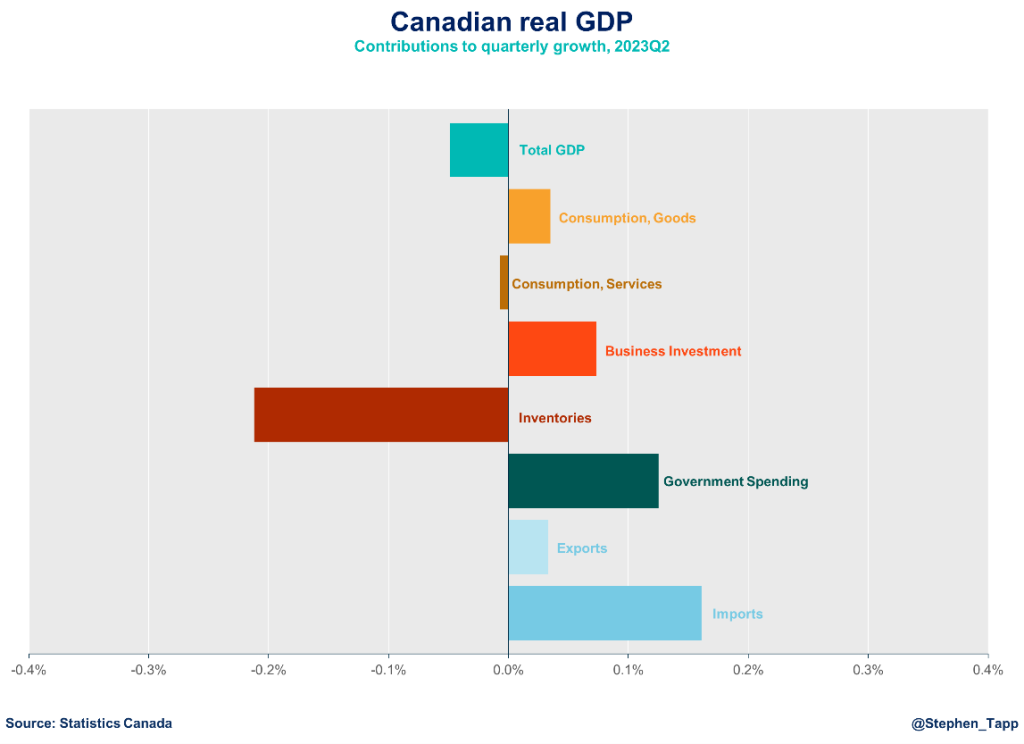

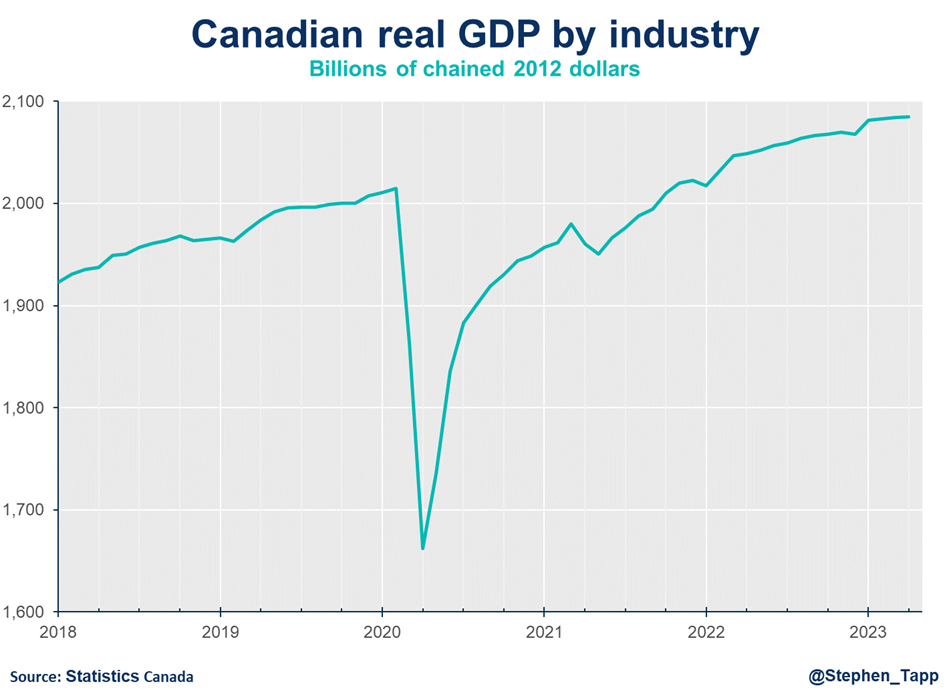

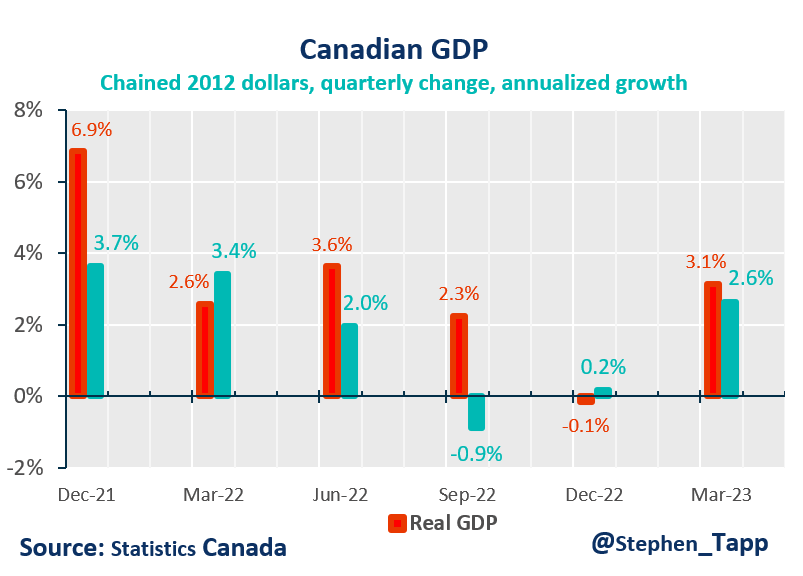

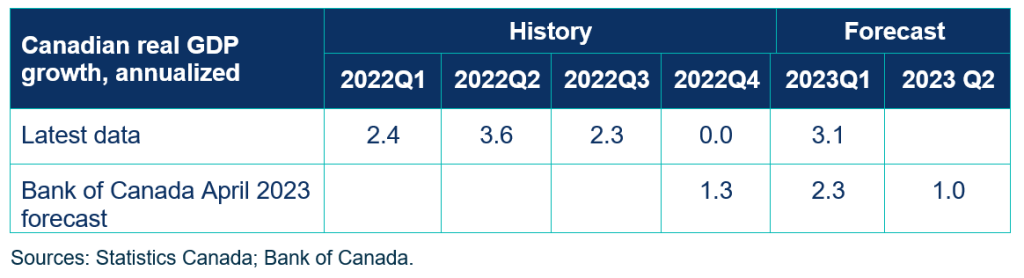

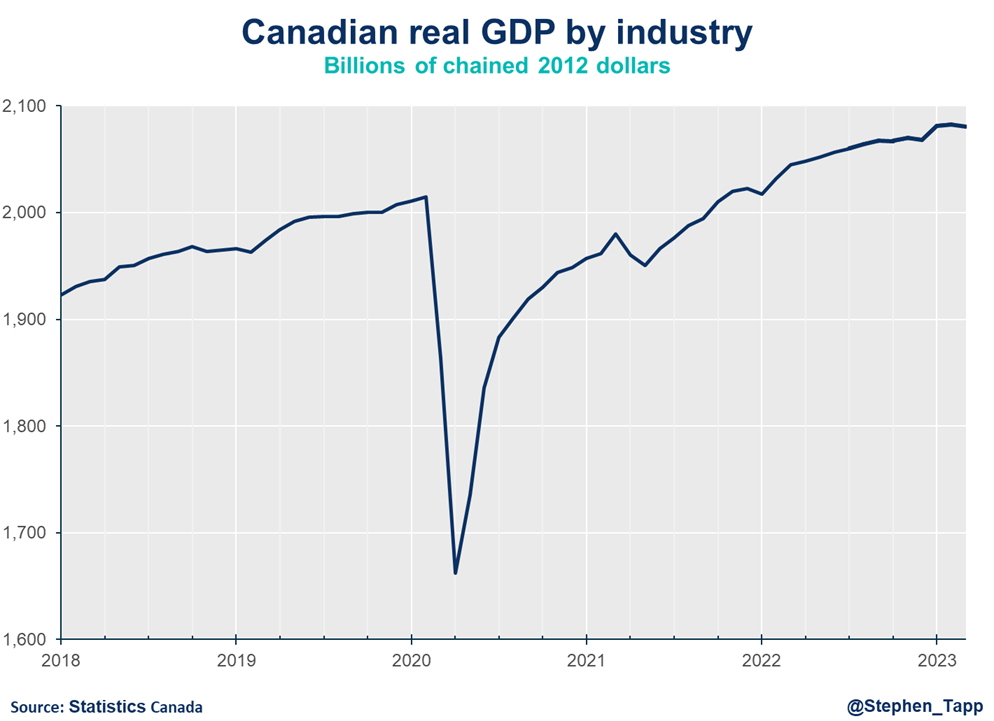

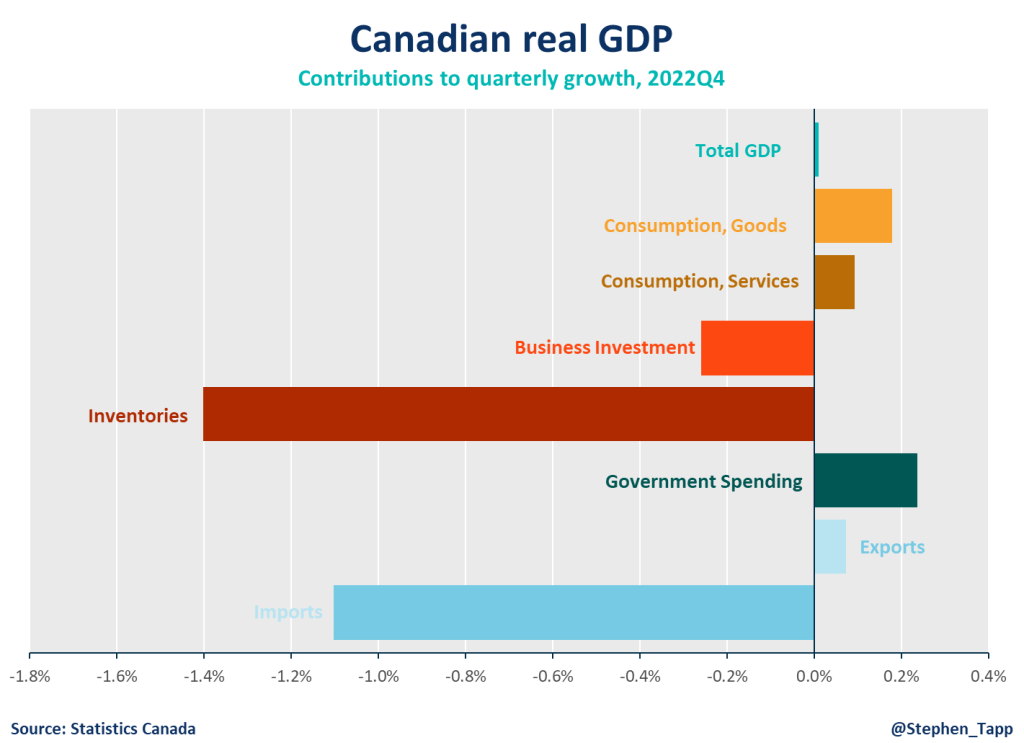

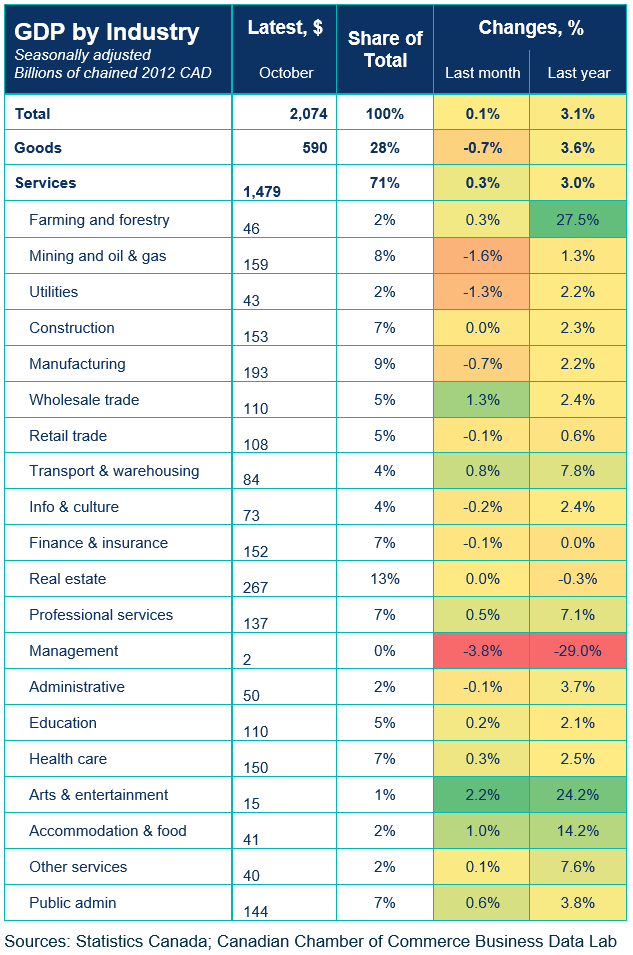

Canada’s real gross domestic product (GDP) growth significantly under-performed expectations witha surprise contraction of 0.2% in the second quarter. This result was much weaker the Bank of Canada’s forecast of a 1.5% gain, and the 1.2% consensus call.

Moreover, growth for Q1 was revised down to 2.6% from 3.1%.

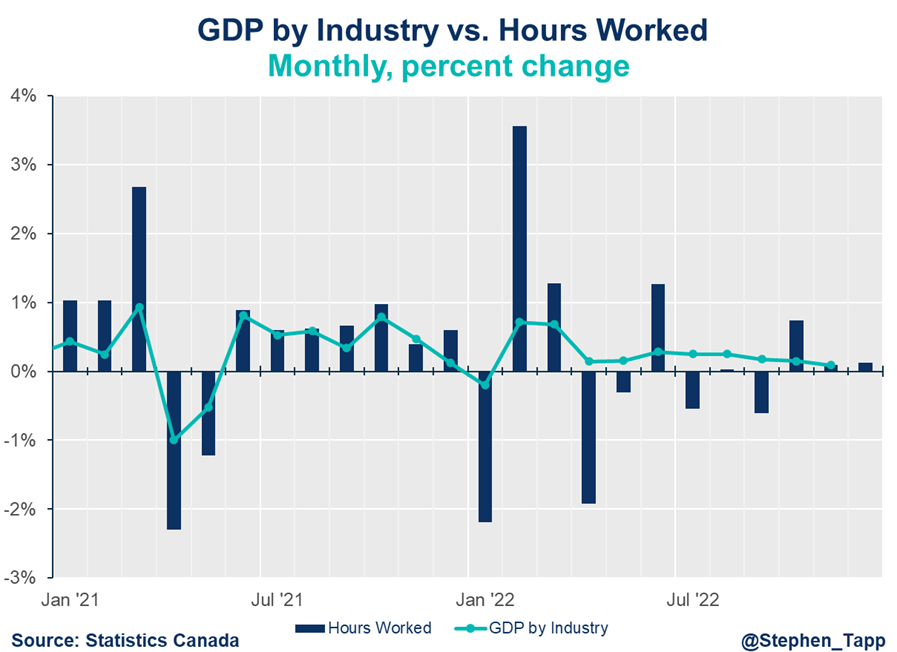

There are now clear signs that higher interest rates are weighing on the economy, as consumers are finally starting to pinch their wallets — consistent with the earlier warnings from our Local Spending Tracker. The slowdown was attributable to household spending (0.1% down from 1.2% last quarter), continued declines in housing investment (-2.1%, for the fifth quarterly decrease!), smaller inventory accumulation, as well as slower export growth (+0.1% following 2.5% increase in Q1 2023). Increased business investment in engineering structures (+3.3%) and higher government spending on wages (+2.2%) were among the few components that aided the economy’s growth.

Movers and Shakers

There was a very modest increase in spending on goods (+0.1%), but the real surprise was the weakness in household spending on services, which was flat in Q2, after a 1.1% increase in Q1.

The report also noted that “while aggregate household expenditures edged up in the second quarter, spending per capita fell 0.7%. In fact, per capita household spending declined in three of the last four quarters.” – again in line with the insights from our spending tracker.

SENTIMENT, OUTLOOK & IMPLICATIONS

Outlook Ahead/Recession Pulse

This represents a clear miss for the second quarter forecast by the consensus market call and the BoC. The only “good news” is that this release should finally cement the case for the Bank of Canada to hold on interest rates next week.

The advanced estimate for July suggests GDP was unchanged on the month. A variety of special, albeit temporary factors —on-going forest fires and a major port strike in July — will hurt activity in the third quarter. All in all, it’s entirely possible that Canada’s economy’s is already in a mild recession.

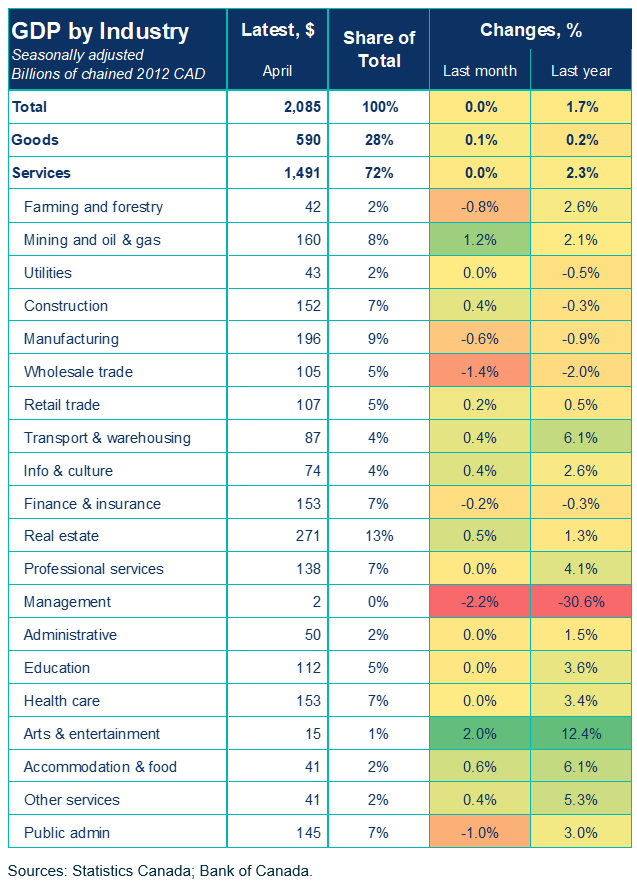

SUMMARY TABLES

Source: Statistics Canada; Bank of Canada.

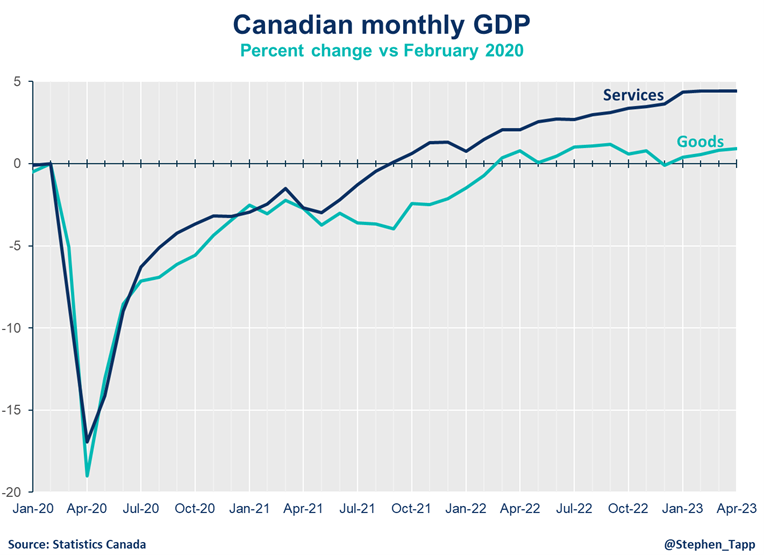

CHARTS

Sources: Statistics Canada; Bank of Canada; Canadian Chamber of Commerce Business Data Lab.

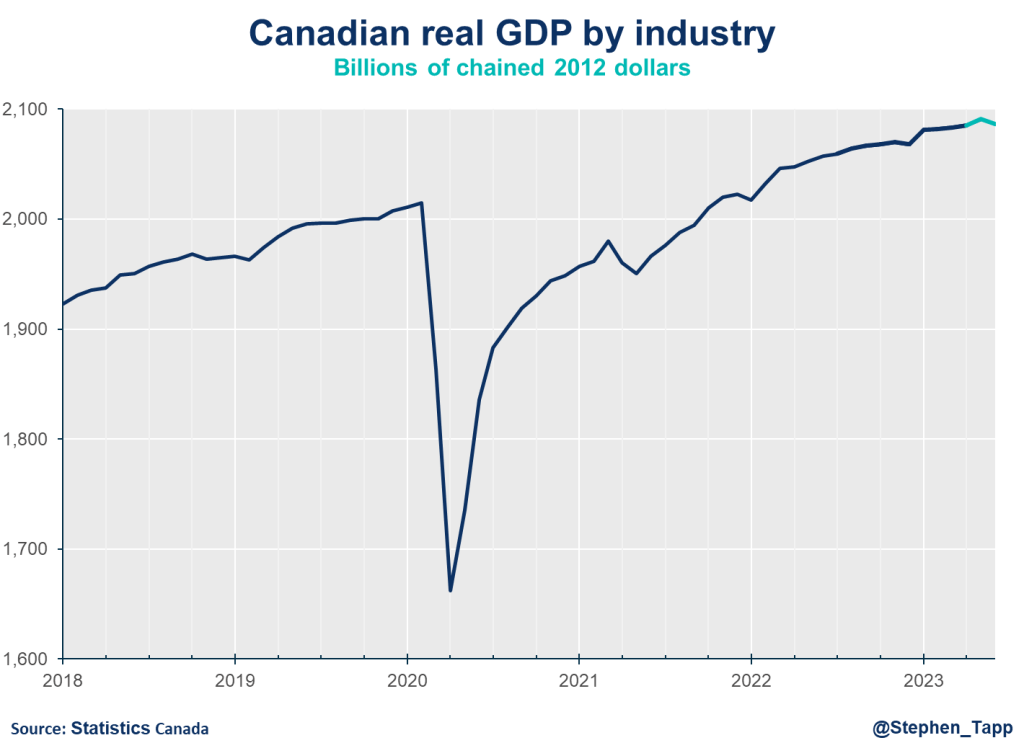

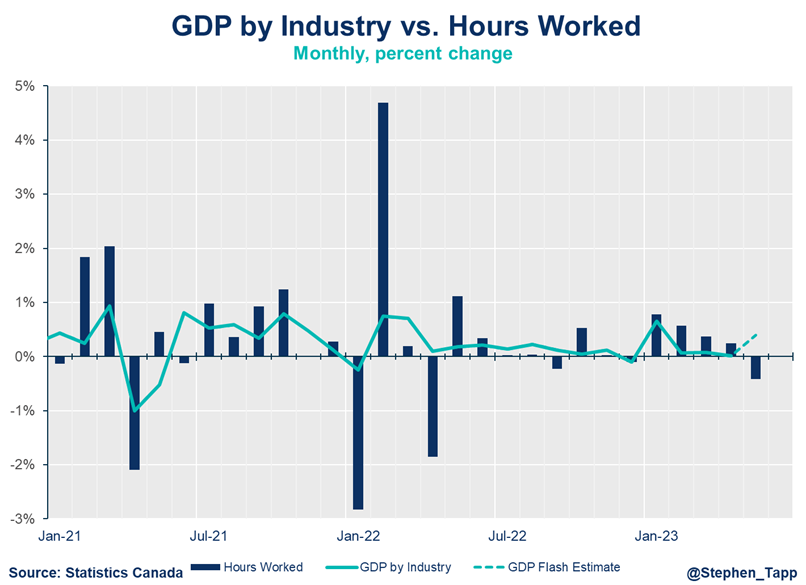

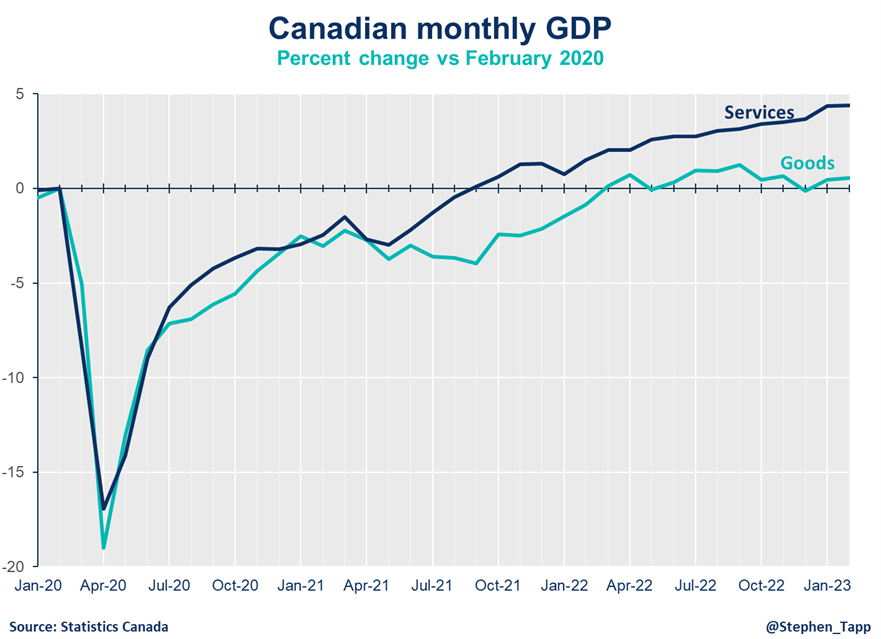

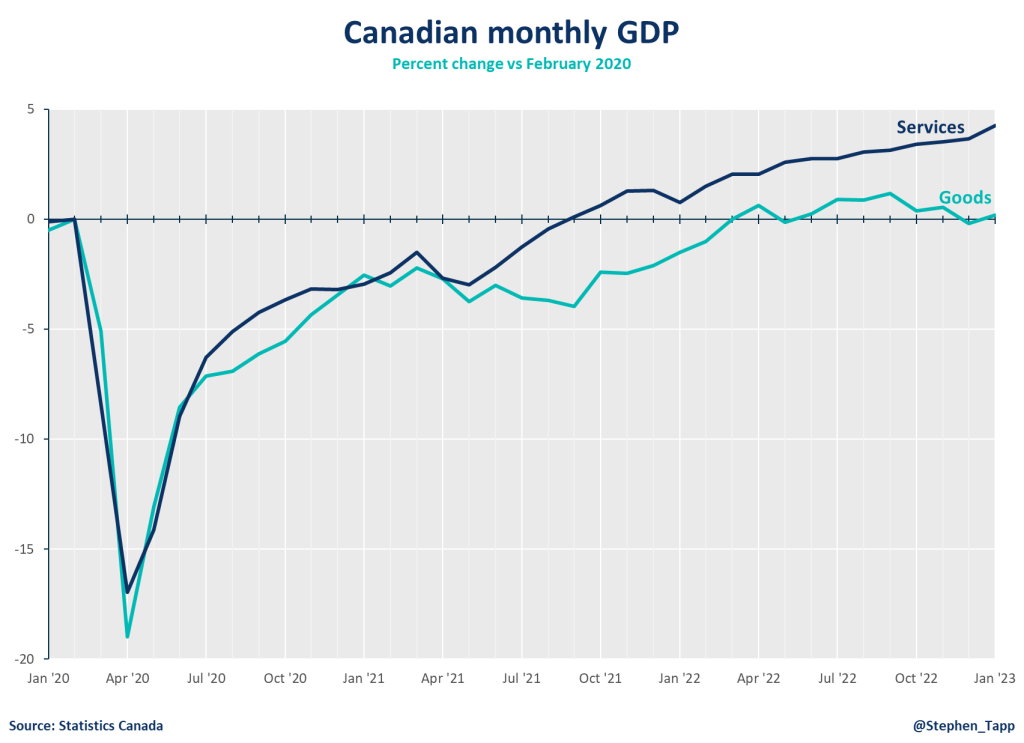

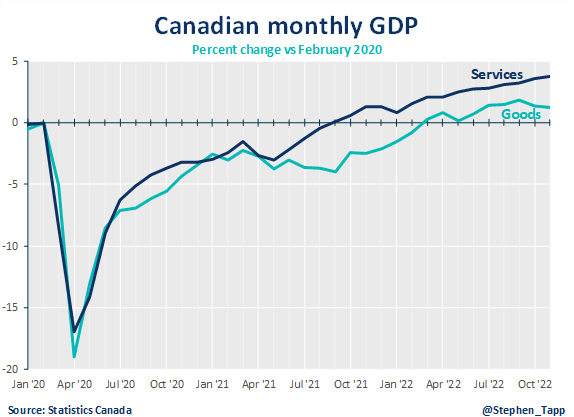

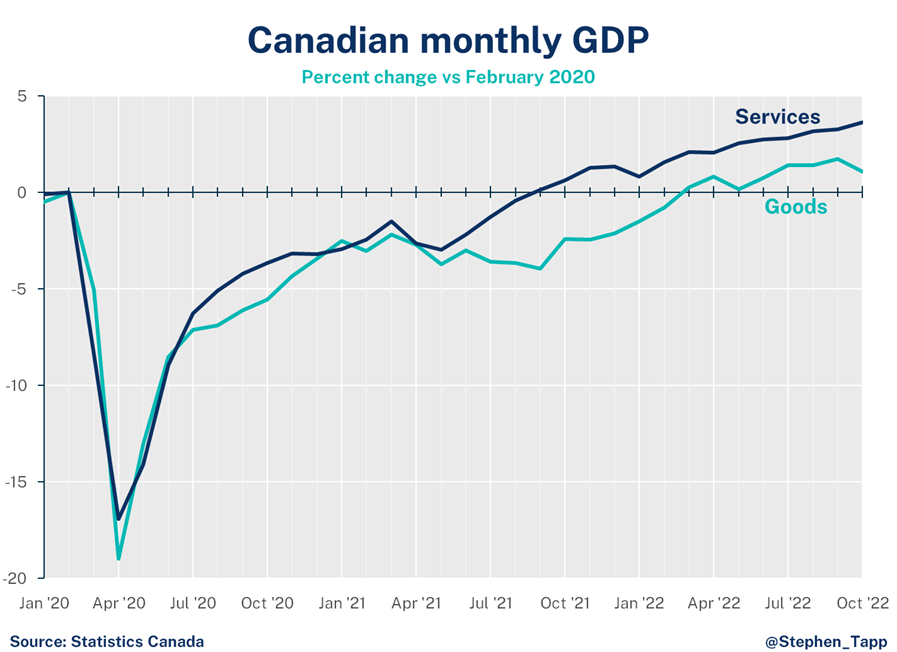

Canada’s GDP rose 0.3% in May, matching market expectations. Output was helped by the easing of supply chain pressures, the end of a federal public servant strike and continued momentum in real estate, but forest fires disrupted Alberta’s oil and gas sector.

Rewa

Canada’s GDP rose 0.3% in May, matching market expectations. Output was helped by the easing of supply chain pressures, the end of a federal public servant strike and continued momentum in real estate, but forest fires disrupted Alberta’s oil and gas sector.

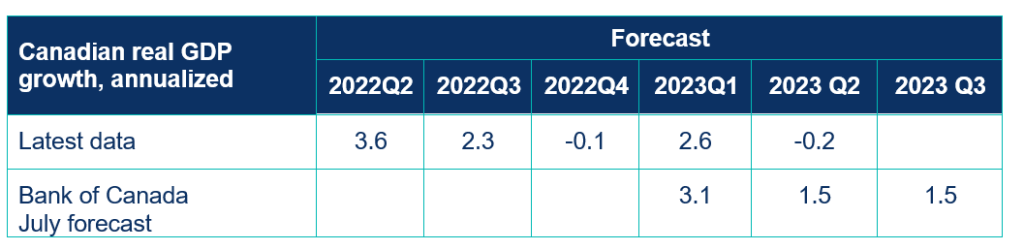

Factoring in StatCan’s flash estimate of a 0.2% drop in June, Canadian real GDP is expected to grow at approximately 1% in the second quarter — down noticeably from over 3% in Q1, slightly weaker than what the Bank of Canada had expected. As a result, we’re becoming more confident that the Bank of Canada will hold its policy rate at 5% in September, marking the peak of this tightening cycle.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headline

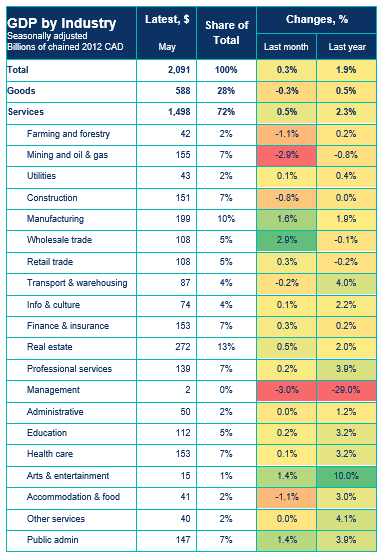

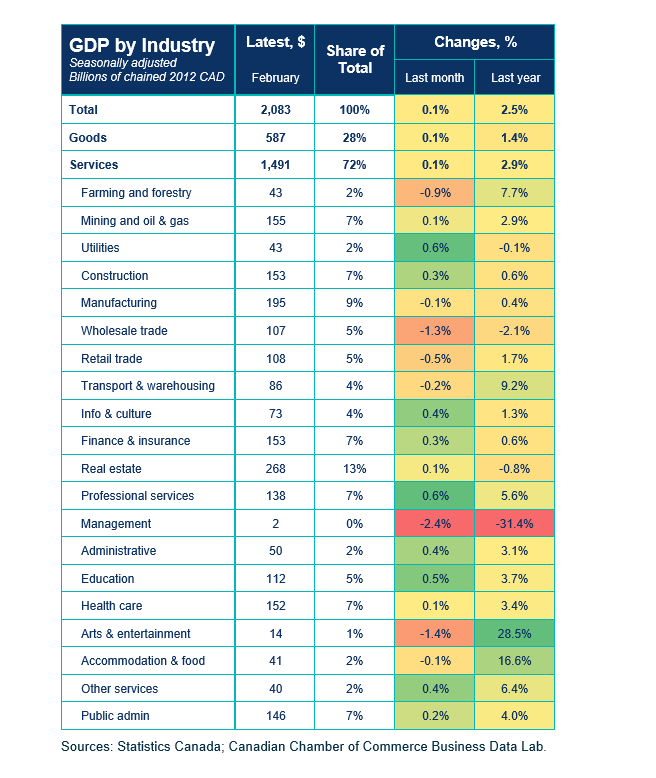

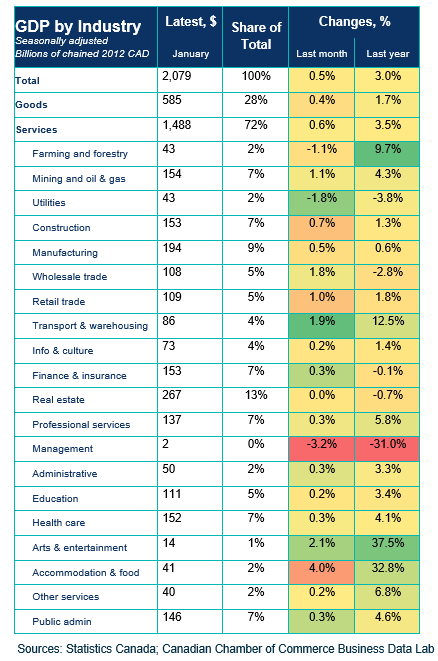

Canada’s real gross domestic product (GDP) was up 0.3% in May, matching market expectations.

Output grew in 12 of 20 sectors, led by gains in services, which were up 0.5% on the month, while the goods sector dropped 0.3%.

Movers and Shakers

As expected, the public sector rebounded in May, following a federal public servant strike of April 19 to May 3, which had temporarily shaved off about 0.1% from the headline GDP number in April.

In May, forest fires disrupted production in Canada’s energy sector (-2.1%). Alberta’s oil and gas in was hit hardest, dropping 6.6% and recording its largest monthly contraction in over three years. While this is a temporary disruption, we know that fires continued beyond May, and may act as a drag on output for a few more months.

The easing of supply chains pressures —with an improved supply of semiconductor chips — helped propel wholesale trade (2.9%) and manufacturing (1.6%).

Improvements in Canada’s real estate sector continue to support GDP, with gains for four consecutive months.

OUTLOOK & IMPLICATIONS

StatCan’s flash estimate for June is -0.2%. This puts Canada’s real GDP on pace for growth of around 1% in the second quarter. This is slightly weaker than the BoC’s latest forecast, which sees growth of 1.5% for both Q2 and Q3, before slowing further for the following three quarters.

The market consensus is slightly weaker than the Bank’s outlook: with growth expected to stall (0%) — but no longer fall — by the fourth quarter, consistent with a much softer landing than was previously expected. All told, the Bank of Canada will likely hold their policy rate at 5%, marking the peak of the tightening cycle.

KEY TAKEAWAYS Headline Movers and Shakers SENTIMENT, OUTLOOK & IMPLICATIONS Outlook Ahead / Recession Pulse SUMMARY TABLE CHARTS Like

Business Data Lab

Today’s report on Canada’s GDP was lackluster at best – as the economy held unchanged (0.0%) from its relatively unchanged March reading (0.1%). Perhaps the biggest proof that we’re not out of the woods yet, was May’s advance reading (0.4%). There was a lot riding on April’s data but while it is a more favourable turn of events in the context of the Bank of Canada’s upcoming announcement in July, the question is to what extent will it weigh on their decision to issue another consecutive hike.

Marwa Abdou, Senior Research Director, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headline

Canada’s real gross domestic product (GDP) was unchanged (0.0%) in April. This outcome is slightly worse than Statistics Canada’s initial advanced estimate of 0.2%.

Output grew in 9 of 20 sectors where gains in the goods sector (0.1%) were offset by the lack of change in the services sector (0.0%).

Increases in mining, quarry and oil and gas extraction were the most notable (+1.2%).

In time for warmer weather (albeit not lately), construction also grew (0.4%) by way of engineering and non-residential activity.

Movers and Shakers

Also broadly anticipated was the growth in real estate, rental, and leasing sector (0.5%). This marked the second quarter of consecutive growth and the sector’s largest uptick since December 2020!

The public sector recorded the largest decline since January 2022 (-1.0%). The federal public servant strike (from April 19-May 3) temporarily shaved off about 0.1% from the headline GDP number in April but will provide a similar rebound in May.

The manufacturing sector also reported a measurable decline (0.6%) – by way of dips in both durable and non-durable goods.

The decline in wholesale trade (-1.4%) weighed mostly in the services sector softness.

SENTIMENT, OUTLOOK & IMPLICATIONS

Outlook Ahead / Recession Pulse

The report showed some cooling in demand, but it will have to be sustained. In its April report, the Bank of Canada forecasted GDP would increase 1% in the second quarter. May’s strong flash estimate (0.4%!) is ahead of market consensus (0.8%), and BoC expectations (almost 1.5% annualized).

With inflation clocking in at 3.4% in May and still hovering above the Bank’s target and the labor market remaining relatively tight, there are still a lot of factors at play for the upcoming July announcement. Taken in sum, it remains uncertain whether this was enough to heed another.

After a surprise uptick in April’s inflation, this much anticipated first quarter GDP reading proves the economy still has some steam left in its engine.

Rewa

After a surprise uptick in April’s inflation, this much anticipated first quarter GDP reading proves the economy still has some steam left in its engine. As we anxiously await the Bank of Canada’s upcoming policy rate decision next week, the possibility of at least another hike becomes more real. While forecasters project a slight slowdown for the remainder of the year, it may take longer than anticipated for the combined effects of monetary policy tightening and rising interest rates to sufficiently dampen excessive demand and restore balance to the economy, albeit at a slower pace than desired.

Marwa Abdou, Senior Research Director, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headline

Canada’s real gross domestic product (GDP) growth in the first quarter of 2023 met the Bank of Canada’s expectations, reaching an annualized rate of 3.1%.

The headline figure surpassed market expectations and the federal agency’s forecast of 2.5%, driven by a significant increase in final domestic demand (+0.7%). This is a notable improvement compared to the zero growth reported in Q4 2022. Additionally, StatsCan’s advanced estimate for April 2023 suggests a 0.2% growth, indicating a stronger start to Q2 than anticipated.

The overheated economy proves it still has skin left in the game, with household spending rose for both goods (+1.5%) and services (+1.3%) after two lackluster quarters. However, the savings rate decreased from 5.8% in Q4 2022 to 2.9%.

Movers and Shakers

Spending on durable goods, such as new trucks and sport utility vehicles, saw a significant increase (+3.3%), while semi-durables, like garments, experienced growth of 4.3%. Non-durables, on the other hand, saw a slight decline (-0.2%). In the services sector, growth was led by food and non-alcoholic beverage services, alcoholic beverage services (+4.4%), and travel expenditures by Canadians abroad (+6.8%).

Favourable international trade contributed to overall growth, with exports of goods and services increasing by 2.4%, led by cars and light trucks. Imports also saw a modest uptick (+0.2%).

There is evidence that interest rate adjustments are having an impact, albeit gradually. Residential investment experienced a significant decline for the third consecutive quarter (-14.6%).

Business investment also weakened (-2.5%) for another quarter, partly due to lower inventories, which experienced the smallest change since Q4 2021, putting some downward pressure on GDP growth.

SENTIMENT, OUTLOOK & IMPLICATIONS

Outlook Ahead/ Recession Pulse

Despite the Bank of Canada’s forecast of a 2.3% GDP increase this quarter, unexpected inflationary pressures in April and a persistently tight labor market with near-record-low unemployment indicate that a few key factors remain unchanged: it will require time, and this stronger-than-expected economy is not yet free from the potential of another interest rate hike.

After a strong start to the year, Canada’s economic growth slowed in February, and likely turned negative in March. Economic momentum is clearly slowing — both in Canada and abroad — as the accumulating impacts of higher interest rates continue to take hold.

Stephen Tapp

After a strong start to the year, Canada’s economic growth slowed in February, and likely turned negative in March. I still expect a decent headline result for Q1 (with roughly 2% growth annualized), but the warning signs for Q2 are piling up. Economic momentum is clearly slowing — both in Canada and abroad — as the accumulating impacts of higher interest rates continue to take hold.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headlines

After strong growth of 0.6% to start the year in January, Canada’s real GDP growth slowed to 0.1% in February. Markets expected a slightly better result (0.2%, after an advanced estimate of 0.3%).

StatCan’s advanced estimate for March has GDP falling 0.1%. This is not good news, however, Canada’s economy is still on pace to record decent headline growth of roughly 2.5% for the first quarter.

Movers and Shakers

Output grew in 12 of 20 sectors. Both services and goods sectors were up by 0.1%, while goods sectors have had a tougher time since last fall.

Professional services (+0.6% monthly growth)continue to lead the economy.

The resilience in construction (+0.3%, up for a second straight month) is impressive, given the large increase in interest rates over the past year. Perhaps pricing in Canada’s housing market has already hit bottom, given on-going supply challenges and strong demand expected from large increases in immigration in recent months.

The public sector grew by 0.2%, and has grown for 13 months in a row. The federal public servant strike will be a drag on output starting in April.

Wholesale (-1.3%) and retail trade (-0.5%) were weak, dragged down by autos and gas station sales.

Implications

The chances of a “soft landing” had increased in recent months, after very strong data for January, and containment of financial market stress, but the warning signs are piling up. Yesterday’s U.S. GDP growth miss for Q1 (1.1% annualized vs. 2.0% expected) may be a sign of what’s to come in Canada in Q2.

The Bank of Canada’s latest forecast has growth of 2.3% for Q1, slowing to 1.0% in Q2. Alternatively, the Federal Budget — which was based on a private sector forecast average from February — had modest negative growth in the first three quarters of this year.

Canada’s economy got off to a healthy start for 2023 with a 0.5% GDP gain in January, following a slight contraction in December.

Mahmoud Khairy

Canada’s economy got off to a healthy start for 2023 with a 0.5% GDP gain in January, following a slight contraction in December. Advanced estimates for February show another increase (0.3%), which puts real GDP growth on pace for a surprisingly strong annualized 2.9% in Q1. So, it looks like the recession will have to wait for another quarter.

While this pace of economic growth is well ahead of the Bank of Canada’s previous forecast of 0.5%, they are unlikely to revise their policy pause just yet. But this does increase the odds that the Bank’s next interest rate move could be a hike, not a cut, as financial markets have been expecting.

Mahmoud Khairy, Chief Economist, Canadian Chamber of Commerce.

KEY TAKEAWAYS

It’s a good start of the year for Canada’s real gross domestic product (GDP) as it rose 0.5% in January, after a mild contraction in December, exceeding the advanced estimate of 0.3%.

There were broad-based gains in both goods (0.4%) and services sectors (0.6%) and across most industries. Arts & entertainment, accommodation & food services, followed by transport & warehousing were the biggest gainers in January.

Wholesale activity rebounded in January to record 1.8%. The imports of industrial machinery, equipment and parts drove the gains related to construction of a new liquified natural gas terminal in B.C.

Mining, quarry and oil and gas extraction has rose by 1.1% in January, led by oil sands extraction. Mining increased by 1.0% due a sharp increase in coal exports to China.

The manufacturing sector grew by 0.5% in January, led by durable goods (1.2%) for the third consecutive month, especially for passenger cars as the easing of supply chain challenges and increased production days contributed to higher production.

The construction sector has its largest gain since March 2022 increasing by 0.7%, with increases in all subsectors, aided by unseasonably warm weather on the month.

Transportation and warehousing started to recover by 1.9% in January after a bad weather caused the sector to contract in December. Rail transportation led the way (12%) with largest growth rate since May 2014.

Accommodation and food services expanded by 4.0% as there was increased activity at restaurants.

Arts, entertainment, and recreation gained 2.1% with increased attendance for hockey games (both NHL and Canada hosting the World Juniors).

The public sector expanded for the 12th consecutive month by 0.3% in January reflecting increase in all subcomponents.

Advanced estimates for February show 0.3% growth. Taken together, these estimates put real GDP growth on an annualized pace of 2.9% for 2023Q1, which is running well ahead the Bank of Canada’s forecast (0.5%) and budget forecast of -0.3%.

The flat GDP growth for the fourth quarter of 2022 is worse than expected, and will have forecasters looking closer to time the start of a potential recession in Canada. The signals from the monthly data point to a strong showing in January, but make no mistake, the economy’s fundamentals are weakening and momentum is slowing as higher interest rates are beginning to bite.

Stephen Tapp

Today’s flat GDP growth for the fourth quarter is worse than expected, and will have forecasters looking closer to time the start of a potential recession in Canada. The signals from the monthly data point to a strong showing in January, but make no mistake, the economy’s fundamentals are weakening and momentum is slowing as higher interest rates are beginning to bite.

– Stephen Tapp, Chief Economist, Business Data Lab, Canadian Chamber of Commerce

KEY TAKEAWAYS

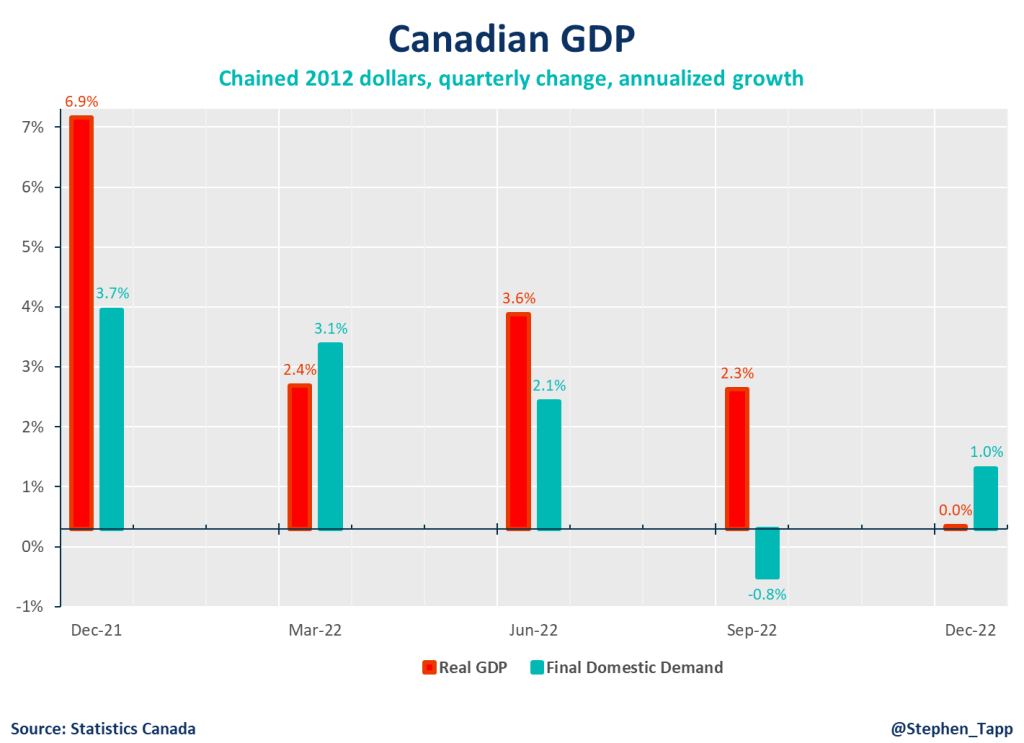

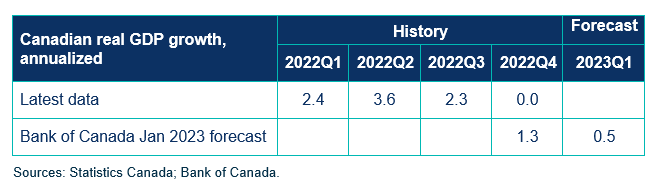

Canada’s real gross domestic product (GDP) growth was flat (0.0% annualized) in the fourth quarter of 2022 — significantly under-performing market expectations (1.3%).

For calendar year 2022, growth was 3.4%. This rate is slower than the 5% recorded in 2021 at the start of the pandemic economic rebound. Most forecasters expect the slowdown to continue into 2023, with growth of less than 1%.

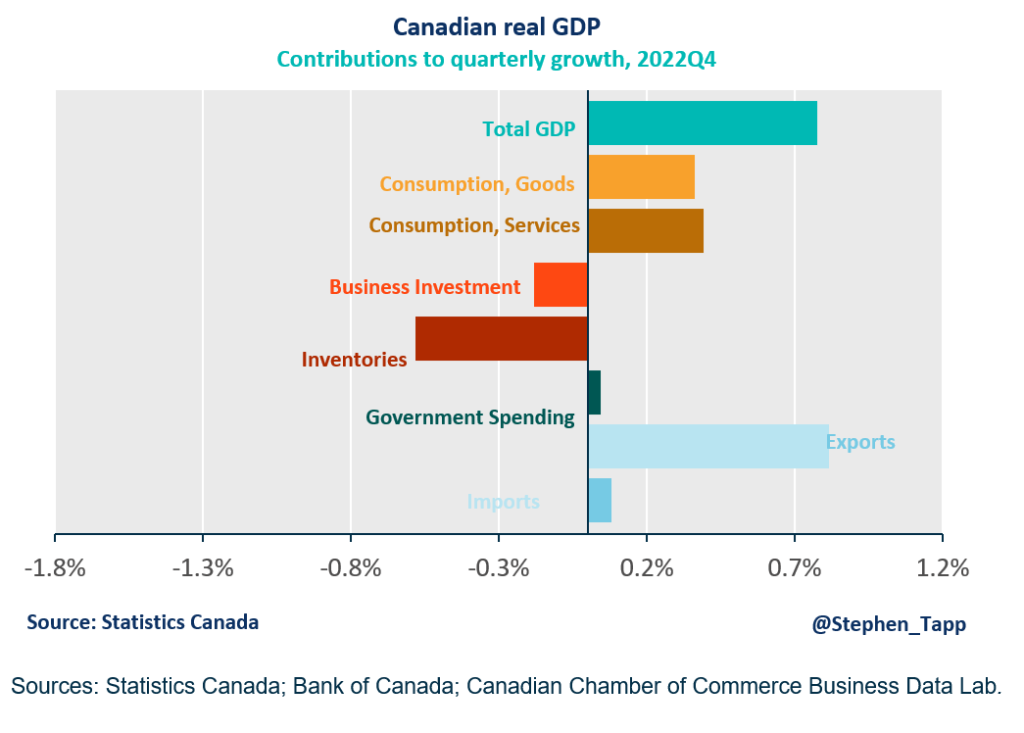

Unlike last quarter, some details are marginally better than the headline figure. In Q3, a buildup of inventories and trade gain flattered headline GDP, but these factors reversed and hurt the headline number in Q4. This can be seen in the fact that final domestic demand rebounded (+1.0% in Q4, after falling 0.8% in Q3).

Consumer spending bounced back (+2.0%, after falling -0.4% in Q3). With the easing of global supply chain problems, goods spending picked up on motor vehicles. Services spending was also positive, but growth slowed as consumers recover from previous spending-sprees following the easing of COVID restrictions. The household saving rate increased from 5.0% to 6.0%, as disposable income was padded by government benefits (a GST credit top-up and Old Age Security payments).

It’s no surprise that sharply higher mortgage ratescontinue to deflate Canada’s housing market, which had boomed earlier in the pandemic. Residential investmentfell for the third consecutive quarter (-9%).

Business investment remains weak (-5%), and has also fallen for three straight quarters, amid higher borrowing costs and a weakening and uncertain sales outlook. Spending on machinery and equipment fell by 28% on the quarter.

International trade: Exports edged up again (+1%) after strong third quarter, but imports were down sharply (-12%), which is not a good sign for business investment or future production.

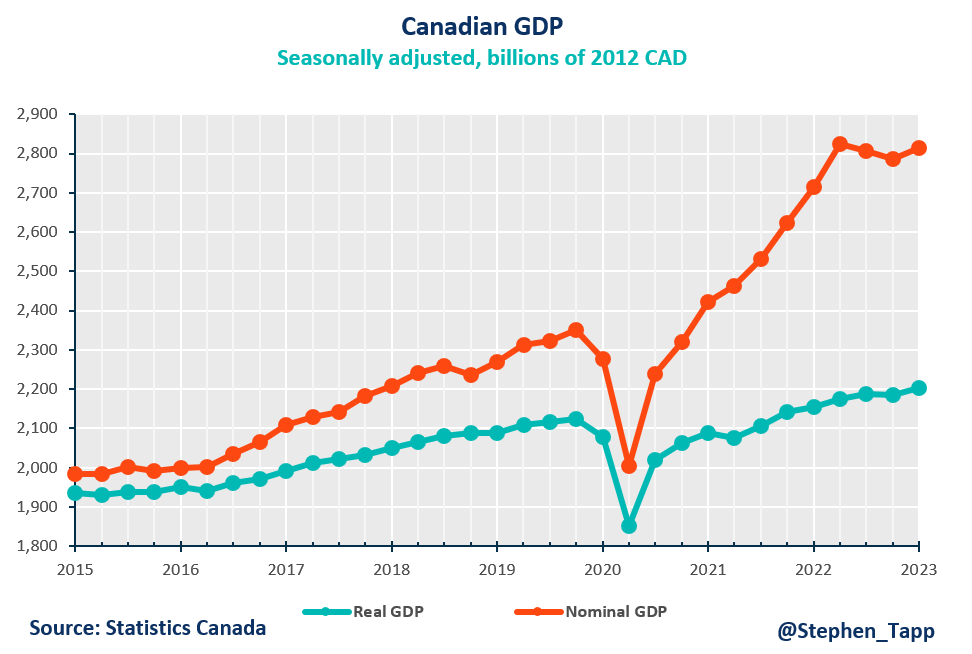

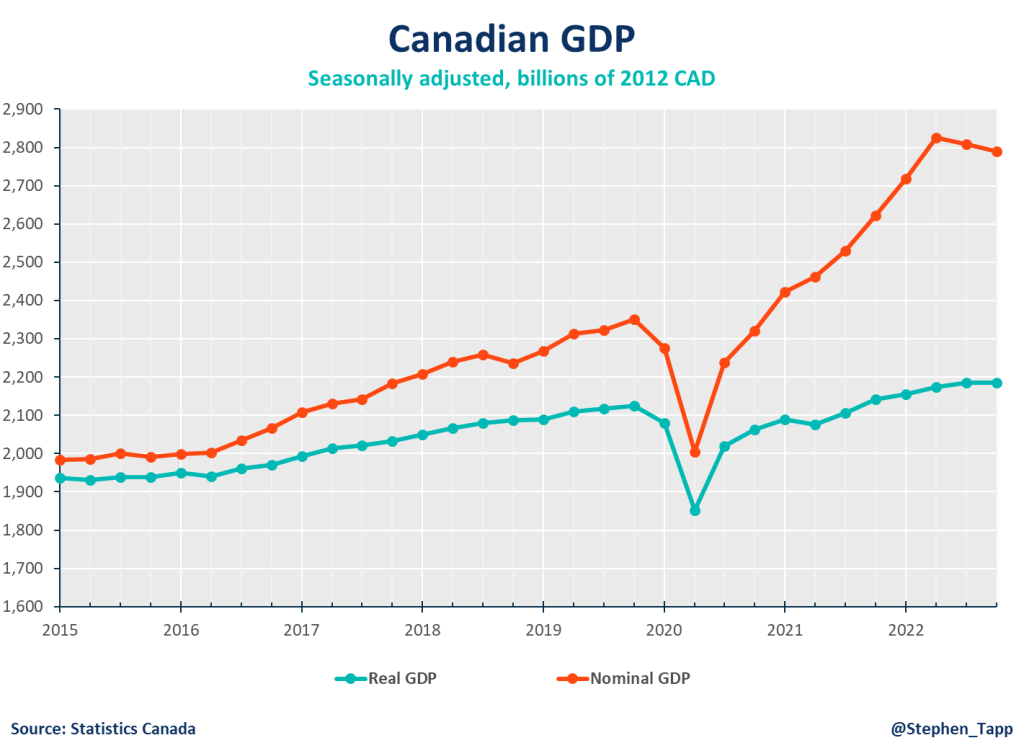

Nominal GDP, which had been doing very well due to rising prices, fell for the second straight quarter (-2.7% annualized in Q4, but +11% for 2022 overall). Canada’s terms of trade continue to fall due to lower energy prices.

Today’s release also includes monthly details for GDP by industry, which shows -0.1% for December (worse than the flash estimate of +0.0%), and is partly attributable to adverse weather that constrained production in oil and gas, transportation and warehousing.

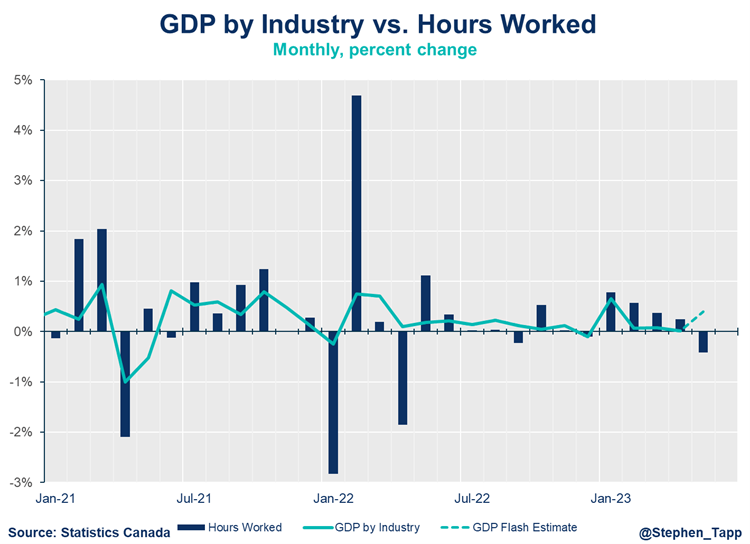

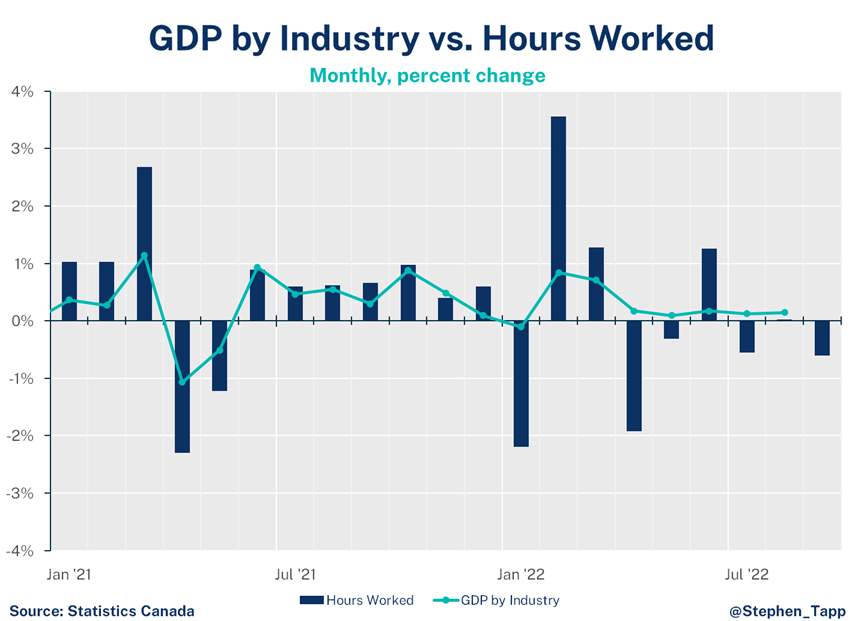

Thankfully, StatCan’s flash estimate for January is a very strong +0.3% rebound, for a month that already had a monster Labour Force Survey featuring an impressive 150k employment gain, and rising hours worked (both +0.8% month-on-month). Assuming no further changes, 2023Q1 growth would be positive +1.0%.

The Bank of Canada’s January forecast acknowledged that two quarters of slightly negative growth are about as likely as two quarters of slightly positive growth. In other words, the Bank continues to put ~50-50 odds on the likelihood of Canada’s economy experiencing a “technical recession” in the short-term.

Today’s GDP data show Canada’s economy is clearly slowing down with a modest 0.1% uptick in November driven by services and aided by the easing of international travel restrictions. Statistics Canada’s advanced estimate shows no change in December, putting annualized real GDP growth on pace for 1.6% in Q4.

Mahmoud Khairy

Today’s GDP data show Canada’s economy is clearly slowing down with a modest 0.1% uptick in November driven by services and aided by the easing of international travel restrictions. Statistics Canada’s advanced estimate shows no change in December, putting annualized real GDP growth on pace for 1.6% in Q4. This is roughly half the pace of Q3’s growth (2.9%). But all things considered, Canada’s economy is still holding up. It’s too early to see a recession yet in these numbers.

Mahmoud Khairy, Economist, Business Data Lab, Canadian Chamber of Commerce

KEY TAKEAWAYS

Canada’s real gross domestic product (GDP) has met initial advanced estimates to grow by 0.1% in November, as output gains in services industries (+0.2%) were dragged down by falling goods production (-0.1%).

Statistics Canada’s advanced estimate shows no change in December. Taken together, these estimates put real GDP growth on an annualized pace of almost 1.6% for 2022 Q4, which is running a little ahead of the Bank of Canada’s forecast (1.3%).

In November, output increased in 14 of 20 sectors. Services led the way rising by 0.3%, due to gains in the public sector, utilities, and arts & entertainment. Goods production fell by0.1% due to declines in machinery production, chemicals, and printing & related activities.

Notable movers of the month:

Finance and insurance started to reverse trend by increasing 0.5% after three months of contraction. The main contribution comes from increases in household mortgage and non-mortgage debt.

The public sector grew by 0.3%, led by both federal government (0.7%) and provincial and territorial public administration (0.7%), while the health care sector and social assistance increased by 0.2%.

Retail activity declined 0.6% in November especially in food and beverages (-1.8%) due to price increases. This decline was partially offset by increased gasoline stations’ activity (+4.2%) due to lower prices in Western Canada caused by reopening refineries.

Accommodation and food services activity is fluctuating in the second half of 2022. It contracted by 1.4% in November after rebounding from the effects of the Omicron variant in the first half of 2022.

Construction fell by 0.7% mainly due to higher interest rates which affected residential construction (-1.8%).

Our Chief Economist reviews Canada's GDP data from October 2022.

Stephen Tapp

Today’s GDP data suggest Canada’s economy continues to outperform low expectations. Real GDP growth is on pace for an annualized +1.4% in 2022Q4, which means earlier recession calls may have to wait until the New Year for resolution.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

Key Takeaways

Canada’s real gross domestic product (GDP) grew by 0.1% in October, as output gains in services were dragged down by falling goods production.This outcome is slightly better than the initial advanced estimate of essentially unchanged growth.

StatCan’s advanced estimate for November is 0.1% growth (which was originally reported as 0%). Taken together, these estimates put real GDP growth on an annualized pace of almost 1.5% for 2022Q4, which is running ahead of the Bank of Canada’s forecast (0.5%).

In October, output increased in 11 of 20 sectors. Services led the way rising by 0.3%, due to gains in the public sector, wholesale, and customer-facing industries. Goods production fell0.7%, due to declines in mining, oil and gas, and manufacturing.

Notable movers on the month:

The recovery in “high-contact services” continues, as Canadians are taking flights (air transport, +5.5%), attending shows (arts, entertainment and recreation, +2.2%), and dining out at restaurants (food services and drinking places, +2.1%).

The public sector grew by 0.4%, led by the federal government (1.0%), while the health care sector (0.3%) responded to additional demand coming from the triple-whammy of COVID-19, respiratory syncytial virus and flu cases.

Wholesale trade (+1.3%) was active, reflecting the processing of new COVID variant boosters as well as farming products, which are supporting strong agricultural exports of wheat and canola this year.

Oil sands extraction fell by 3.9% due to scheduled maintenance that interrupted production.

Manufacturing (-0.7%) suffered its fourth decline in six months, falling to the lowest output level since December 2021.

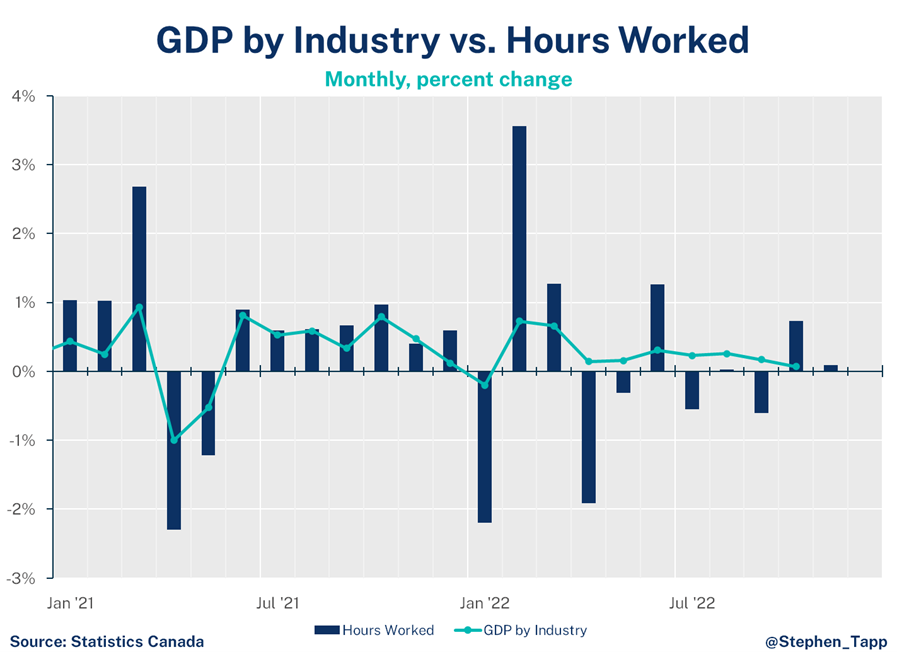

Stephen Tapp, our Chief Economist, analyzes Canada’s real GDP for August, which grew by 0.1%. He highlights that it looks as if Canada’s economy is showing signs of slowing down in the second half of the year.

Stephen Tapp

Canada’s real GDP grew by 0.1% in August, led by gains in services, with the advanced estimate for September showing yet another modest gain (0.1%). Taken together, real GDP is growing at an annualized pace of 1.6% in 2022Q3. This is roughly half the pace of the previous quarter, which shows that Canada’s economy is clearly slowing down in the second half of the year. However, despite all the recession worries, growth remains in positive territory for now, although we expect things to be even weaker in the fourth quarter.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

Canada’s real gross domestic product (GDP) grew by 0.1% in August, led by services sectors. This result was a slight improvement on the initial advanced estimate for essentially flat growth.

StatCan’s advanced estimate for September shows another modest increase of 0.1%. These estimates put real GDP growth on pace for an annualized 1.6% in 2022Q3. This pace is inline with the Bank of Canada’s forecast released earlier this week. These numbers show that overall economic growth in Canada is slowing in the second half of the year, and growth expected to be even slower in the fourth quarter.

Output rose in August in 14 of 20 sectors. Services sectors led the way rising by 0.3%,while goods were down 0.3% due to declines in manufacturing, oil and gas extraction, and construction.

The biggest movers on the month were:

Agriculture (+3.9%)wasled by an increased crop production, as wheat and other grains have benefitted from improved growing conditions in Western Canada this summer.

Utilities (1.5%) rose thanks to gains in electric power generation and natural gas distribution.

Retail trade (+1.2%) and wholesale trade (+0.9%) both performed well.

Construction (-0.7%) fell for the fifth month in a row. All components have weakened, from engineering to residential, non-residential, and repairs.

Manufacturing (-0.8%) had its fourth decline in five months falling to the lowest output level since January 2022.