April 2023 GDP: Canada’s Economy Stalls, May Advanced Estimate Shows Strength: How Long Will It Last?

April 2023 GDP: Canada’s Economy Stalls, May Advanced Estimate Shows Strength: How Long Will It Last?

KEY TAKEAWAYS Headline Movers and Shakers SENTIMENT, OUTLOOK & IMPLICATIONS Outlook Ahead / Recession Pulse SUMMARY TABLE CHARTS Like

Business Data Lab

Today’s report on Canada’s GDP was lackluster at best – as the economy held unchanged (0.0%) from its relatively unchanged March reading (0.1%). Perhaps the biggest proof that we’re not out of the woods yet, was May’s advance reading (0.4%). There was a lot riding on April’s data but while it is a more favourable turn of events in the context of the Bank of Canada’s upcoming announcement in July, the question is to what extent will it weigh on their decision to issue another consecutive hike.

Marwa Abdou, Senior Research Director, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headline

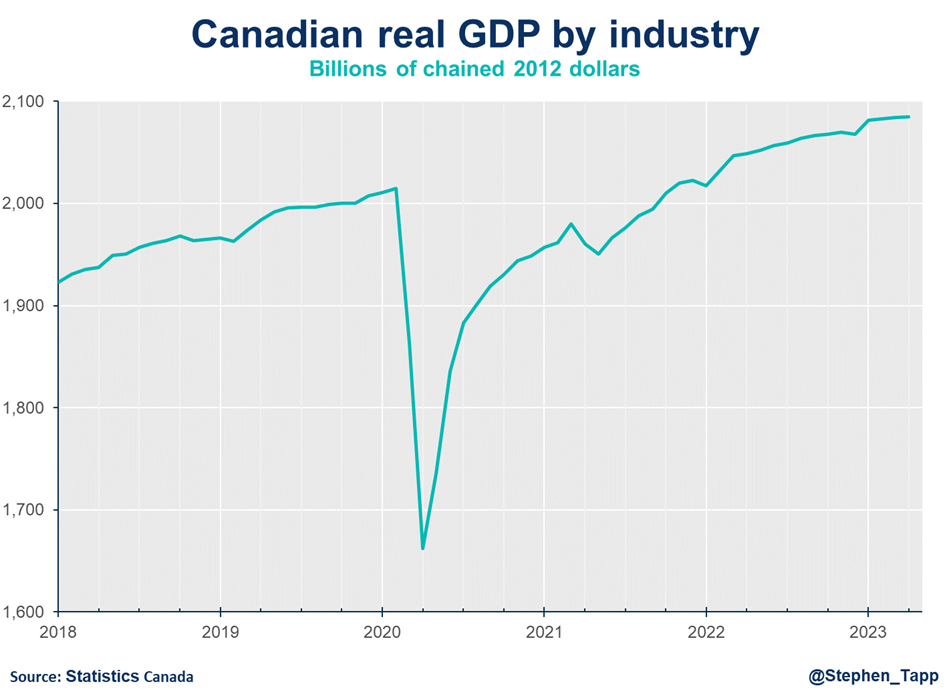

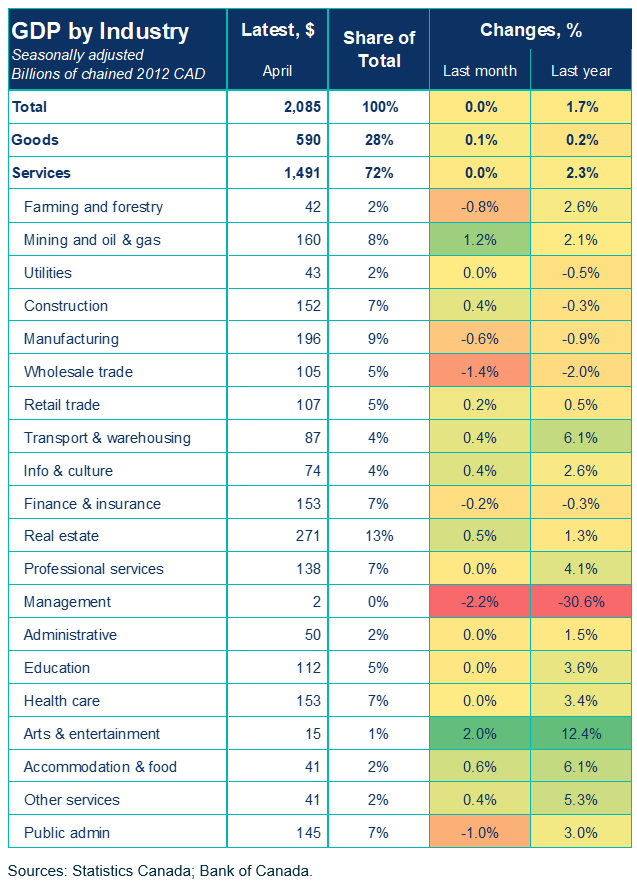

Canada’s real gross domestic product (GDP) was unchanged (0.0%) in April. This outcome is slightly worse than Statistics Canada’s initial advanced estimate of 0.2%.

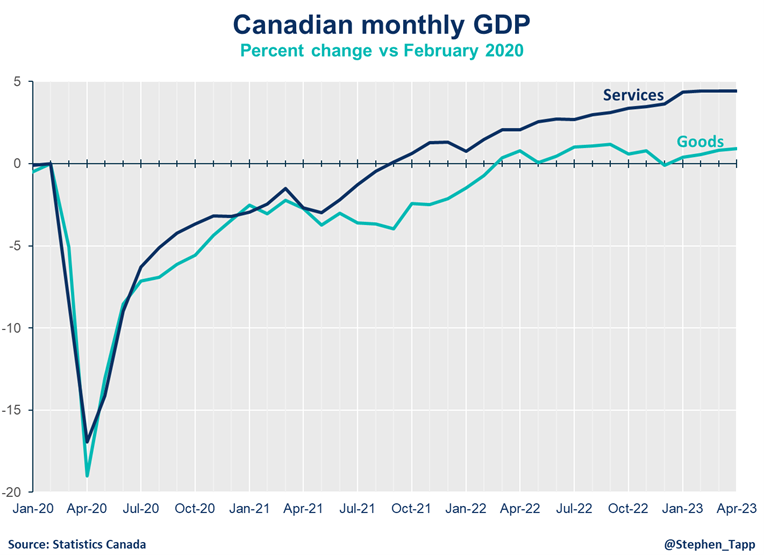

Output grew in 9 of 20 sectors where gains in the goods sector (0.1%) were offset by the lack of change in the services sector (0.0%).

Increases in mining, quarry and oil and gas extraction were the most notable (+1.2%).

In time for warmer weather (albeit not lately), construction also grew (0.4%) by way of engineering and non-residential activity.

Movers and Shakers

Also broadly anticipated was the growth in real estate, rental, and leasing sector (0.5%). This marked the second quarter of consecutive growth and the sector’s largest uptick since December 2020!

The public sector recorded the largest decline since January 2022 (-1.0%). The federal public servant strike (from April 19-May 3) temporarily shaved off about 0.1% from the headline GDP number in April but will provide a similar rebound in May.

The manufacturing sector also reported a measurable decline (0.6%) – by way of dips in both durable and non-durable goods.

The decline in wholesale trade (-1.4%) weighed mostly in the services sector softness.

SENTIMENT, OUTLOOK & IMPLICATIONS

Outlook Ahead / Recession Pulse

The report showed some cooling in demand, but it will have to be sustained. In its April report, the Bank of Canada forecasted GDP would increase 1% in the second quarter. May’s strong flash estimate (0.4%!) is ahead of market consensus (0.8%), and BoC expectations (almost 1.5% annualized).

With inflation clocking in at 3.4% in May and still hovering above the Bank’s target and the labor market remaining relatively tight, there are still a lot of factors at play for the upcoming July announcement. Taken in sum, it remains uncertain whether this was enough to heed another.