Commentaries /

June 2023 LST: Consumers are still spending, but recent rate hikes may be starting to bite

June 2023 LST: Consumers are still spending, but recent rate hikes may be starting to bite

Canadian consumers kept spending in the second quarter of 2023, continuing a trend of resilience in the face of higher interest rates and affordability challenges.

Rewa

Canadian consumers kept spending in the second quarter of 2023, continuing a trend of resilience in the face of higher interest rates and affordability challenges. That said, if there’s a cause for concern in our latest data reading, it’s the fact that spending turned a corner after the Bank of Canada resumed its interest rate hikes in early June. Will this summer finally mark a turning point for Canadian consumers and Canada’s economy more generally? Forecasters have repeatedly pushed off the timing for a recession, as consumers, labour markets and housing have surprised on the upside. Looking ahead, we expect consumer spending to slow noticeably in the second half of the year, as people cut back on discretionary purchases.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

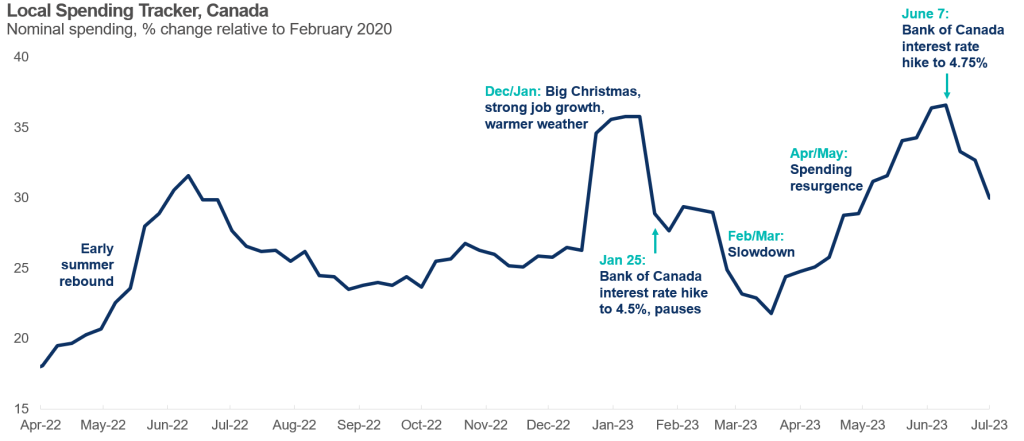

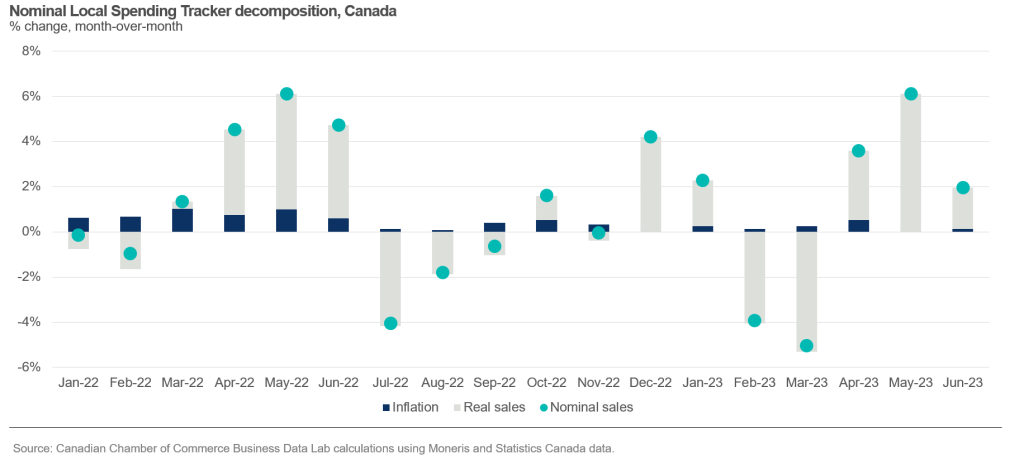

- National spending trends: Our high-frequency weekly spending data show a burst of activity before Christmas that carried into January — supported by a large increase in employment and unseasonably warm weather. By the end of January, the Bank of Canada raised its policy interest rate to 4.5%, and paused further increases.

Our tracker shows consumer spending sagged in February and March. However, consumers opened their wallets by the middle of April through to mid-June. In our data, May enjoyed the fastest pace of nominal spending growth in 12 months. June’s performance was also solid (+2% month-over-month), but momentum clearly slowed over the month.

The is noteworthy because on June 7, the Bank of Canada raised rates by 25 basis points, ended their “conditional pause”, and followed that with another hike on July 12, citing “more persistent excess demand” and inflationary pressures.

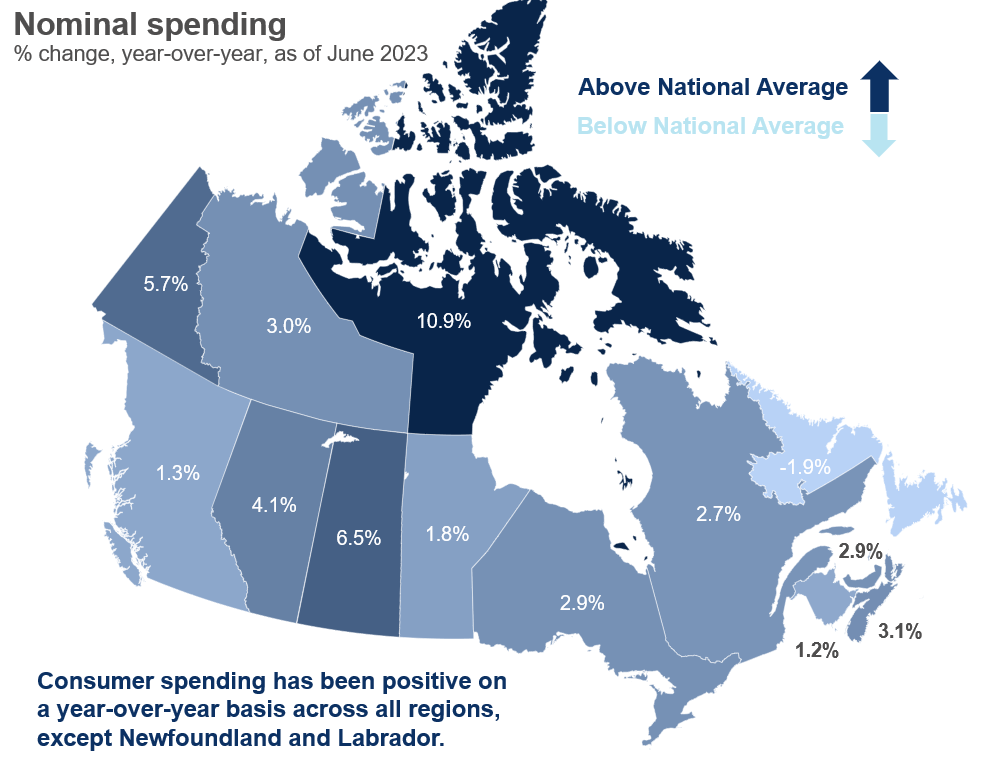

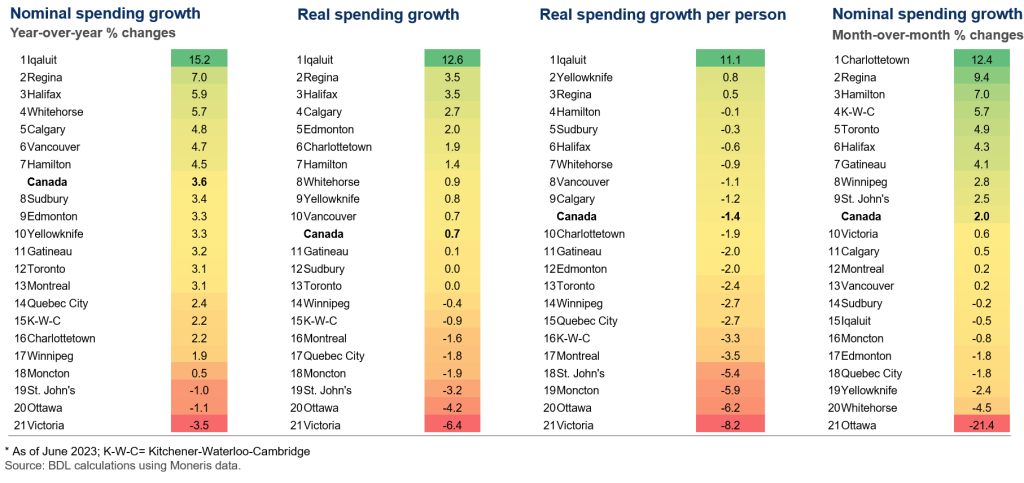

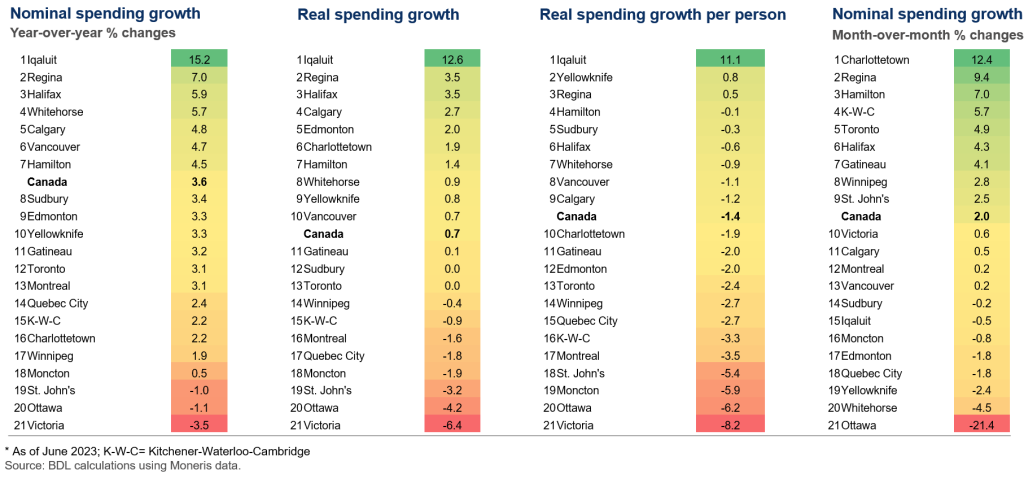

Resilient consumers have been supported by tight labour markets, which are providing full-time jobs and rising wages. Most households built up significant savings buffers during the pandemic, which they’re now using to fulfill pent-up demand for services like vacations, restaurants, and entertainment. - Regional results: Consumer spending stayed positive on a year-over-year basis across all regions of the country, except Newfoundland and Labrador.

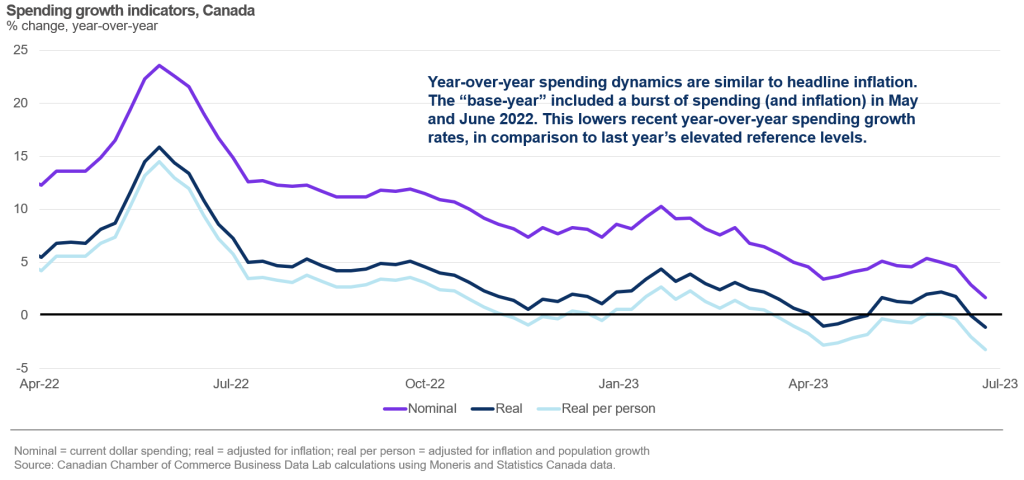

That said, there’s a caveat that our year-over-year spending dynamics are similar to those of headline CPI inflation. Our data are also impacted by “base-year effects”, which included a boom of both inflation and spending in May and June 2022. This tends to lower recent year-over-year spending growth rates, when compared to last year’s elevated reference levels.

Within the country, there are concentrated pockets of spending strength in the Prairies (Alberta, Saskatchewan, and more recently Manitoba), Atlantic Canada (Prince Edward Island, and Nova Scotia) as well as the Territories.

At the other end of the spectrum, spending is soft in Central Canada (Ontario and Quebec), and on the West and East coasts (British Columbia and Newfoundland and Labrador).

Adjusting for inflation and population: Nominal consumer spending is up 3.6% year-over-year in June. Adjusting for inflation, real consumer spending growth remained positive year-over-year (0.7% nationally and up in 8 of 13 regions).

Rapid population growth is also supporting spending. After adjusting for inflation and population, real spending growth per person has been negative since mid-March: it’s down 1.4% nationally year-over-year, and is only positive in 3 of 13 regions, a similar situation to real GDP per person which has continually disappointed.

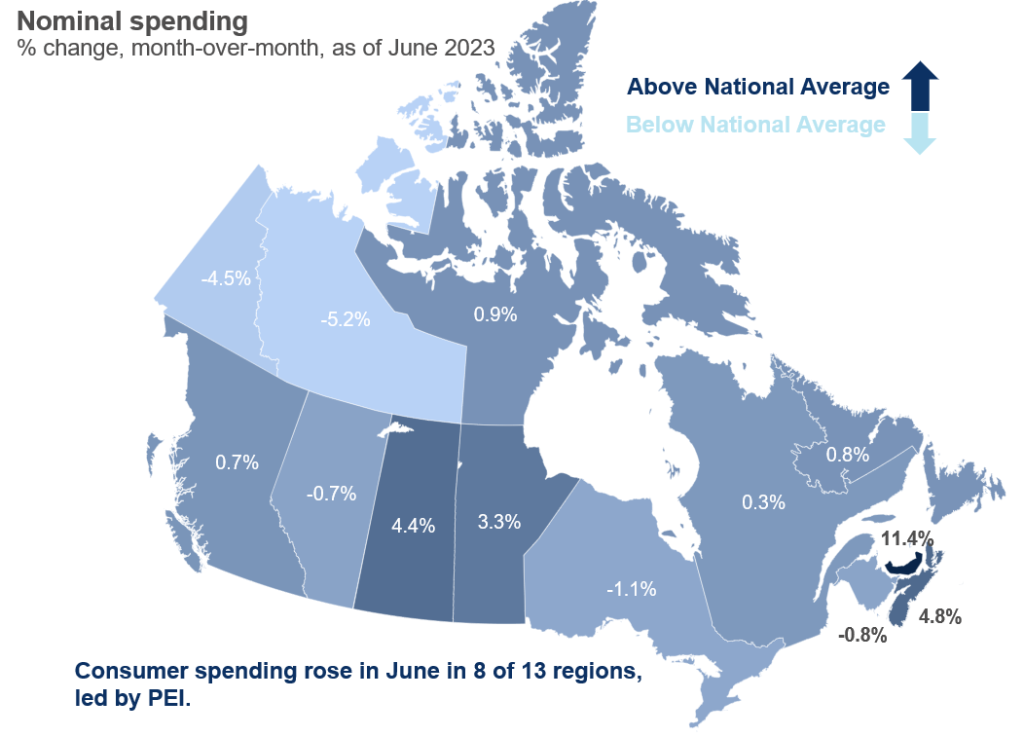

For the month of June: Focusing on shorter-term signals, nominal spending rose 2% in Canada on the month and was up in 8 of 13 provinces/territories, led by PEI (11.4%), Nova Scotia (4.8%), Saskatchewan (4.4%) and Manitoba (3.3%).

- CMA results: Nominal sales rose in June in 13 of the 21 cities we track. Standouts include big cities in the regions leading the country, namely Regina, Halifax, Calgary and Charlottetown.

Ottawa, St. John’s, Victoria and Moncton are lagging behind — however, at least for Ottawa and Moncton, this likely reflect base-effects from strong spending a year ago. - Tomorrow, Statistics Canada releases retail sales for May. Their advance estimate also suggests continued strength with a nominal monthly gain of 0.5%.

MORE CHARTS

RANKINGS

Provinces and Territories

CMAs/ Cities

Other Commentaries

September 2022 Consumer Price Index data: Food and services prices still rising, no progress on core inflation

August 2022 Consumer Price Index data: Finally some good news on Canadian inflation.